Achieve financial well-being with the help of investing

This post has been brought to you in partnership with BlackRock Canada. All thoughts and opinions are my own and do not necessarily reflect the views of BlackRock Canada.

Now that we’re a month into 2018 and your health and fitness resolutions aren’t as top of mind, it’s a good opportunity to evaluate your financial situation. Taking stock of your financial literacy, re-evaluating financial goals and identifying how to achieve them are important steps to take each year.

For anyone looking to set themselves up for long-term financial viability, truly making the most of your money means that investing can’t just be part of a plan, there needs to be action.

Investing: One of the best ways to build wealth over time

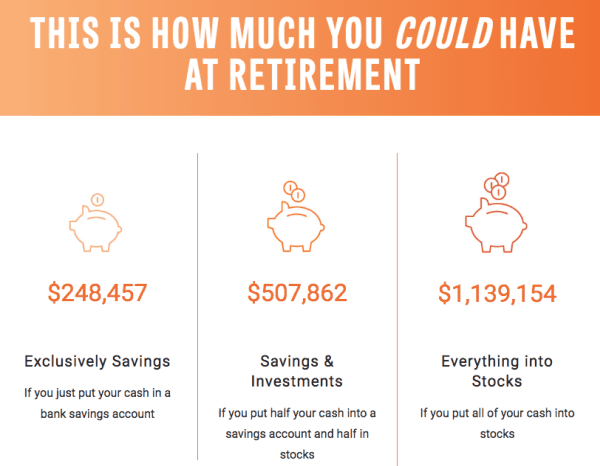

The truth is that investing is one of the best ways to build wealth over time. When you invest, you put your money to work on your behalf. Compounding returns leads to the growth of your portfolio. Let’s be real: you can put money into a traditional savings account for decades, and still not have enough to retire. You need the returns of the market to maximize your money.

This Retirement Income Calculator shows how much you will need to save each year based on your expected rate of return.

That’s a huge difference.

You won’t come close to reaching any sort of retirement goal if you just put your money in a savings account. Plus, inflation is likely to erode your real returns which can also mean that the money you save won’t go as far.

Investing can help you create a nest egg that overcomes inflation risk and can help you create a portfolio that is more likely to help you outlast your money. Without investing, it will be difficult to meet many of your long-term goals — and you might not achieve financial wellness today.

Start investing now to build security later

According to a report from Statistics Canada released last year, almost two-thirds of Canadians (65.2 percent) are saving for retirement, showing that retirement planning is top of mind for many Canadians. The good news is that you don’t need a ton of money to start investing. There are plenty of ways to begin building your nest egg without a huge amount of initial capital. This is a big deal, especially when it comes to retirement.

One of the best strategies to use is called dollar-cost averaging. With this strategy, you figure out how much you can invest each month. Maybe, at first, you feel like you can only set aside $50 or $100 a month. That amount probably won’t allow you to meet your retirement portfolio goals, however, it does help you get in the habit of investing. And besides, the longer your money is in the market, the better off you are likely to be — even if it’s a small amount of money to begin with.

You can use your regular investment to buy shares of ETFs that have exposure to a wide swath of the market. Like mutual funds, ETFs are a diversified mix of stocks and bonds. However, they are traded like stocks on an exchange, making them simple to use. Plus, because holdings are disclosed daily, you can see exactly what you have.

If you feel like you’re hearing more and more about ETFs lately, it’s no surprise. ETFs globally have become an increasingly popular investment tool. In fact, BlackRock’s iShares business expanded at the fastest pace ever last year collecting a record US$246 billion in new flows, taking the global exchange traded fund (ETF) industry beyond US$4.5 trillion in total AUM for the first time. Here in Canada, assets under management grew 22.6 percent organically.

Another nice benefit of investing using ETFs is that you have access to low-cost options. Fees are relatively low, and that means more of your money goes toward building wealth. For some investors, it can make sense to start with iShares Core ETFs to build a portfolio that includes Canadian, U.S., and international stocks. You can get diversity for a relatively small cost.

No matter how much you can set aside, it makes sense to start as soon as possible. Over time, you can increase the amount you invest. In fact, if you start with a small amount, it makes sense to plan to increase the amount you invest so that you don’t end up falling behind. Make it a habit, and then begin investing more over time.

Take advantage of registered accounts

The Canadian government is pretty good at encouraging you to invest. There are ways to invest to save for a number of goals. You can use an RRSP to save for retirement. An RESP can help you save money for your child’s college with the help of investing. Finally, the TFSA can hold investments that can help you reach just about any other goal you have.

Your financial well-being should include a plan to use tax-advantaged investment accounts to maximize the efficiency of your money over time. The less you pay in taxes on the money, the better it grows over time.

Figure out what you need to invest to reach your retirement goal, and then if you have leftover money, invest it using your TFSA or put it in an RESP for your kids. Either way, this can be a great way to build for future goals while enjoying peace of mind today.

Holistic financial wellness

It’s a great time of year to hit pause and re-focus on holistic financial wellness. Too often, we get caught up in what is happening now. While short-term expenses and financial obligations are important to plan for, and you might have debt to tackle, the reality is that you can’t let it prevent you from looking to the future.

Think about your finances as a whole, and pay attention to what you can do to integrate long-term goals with your short-term financial needs. In some cases, you might need to turn to a financial planner to help you figure this out. However, the important thing is to make a plan, and then to tweak it over time as your situation changes.

Even if you are focused on paying down debt, you can still look into investing. Setting aside a small amount each week can still be a big deal down the road. Take a look at your financial wellness from a big picture angle to help you make the most of your money today — and tomorrow.